If you have just built a metal building, metal garage, steel shed, metal barn, or detached workshop, one of the most important next steps is making sure it is properly insured.

A lot of homeowners already have some coverage for detached buildings under their existing homeowners policy. In many cases, that coverage appears under Coverage B, often called Other Structures. This part of the policy typically applies to structures on the property that are not attached to the main house, such as detached garages, sheds, shops, and similar outbuildings.

That matters for anyone building a custom metal building, because many property owners assume the building is fully insured automatically. Sometimes it is. Sometimes it is only covered up to a certain amount, and that amount may not be enough to rebuild the structure after a loss.

The short answer

Yes, a homeowners policy may already insure a detached metal building on your property. But the key questions are:

- Does your policy include Other Structures coverage?

- How much coverage is included?

- Is that amount enough to rebuild your metal building today?

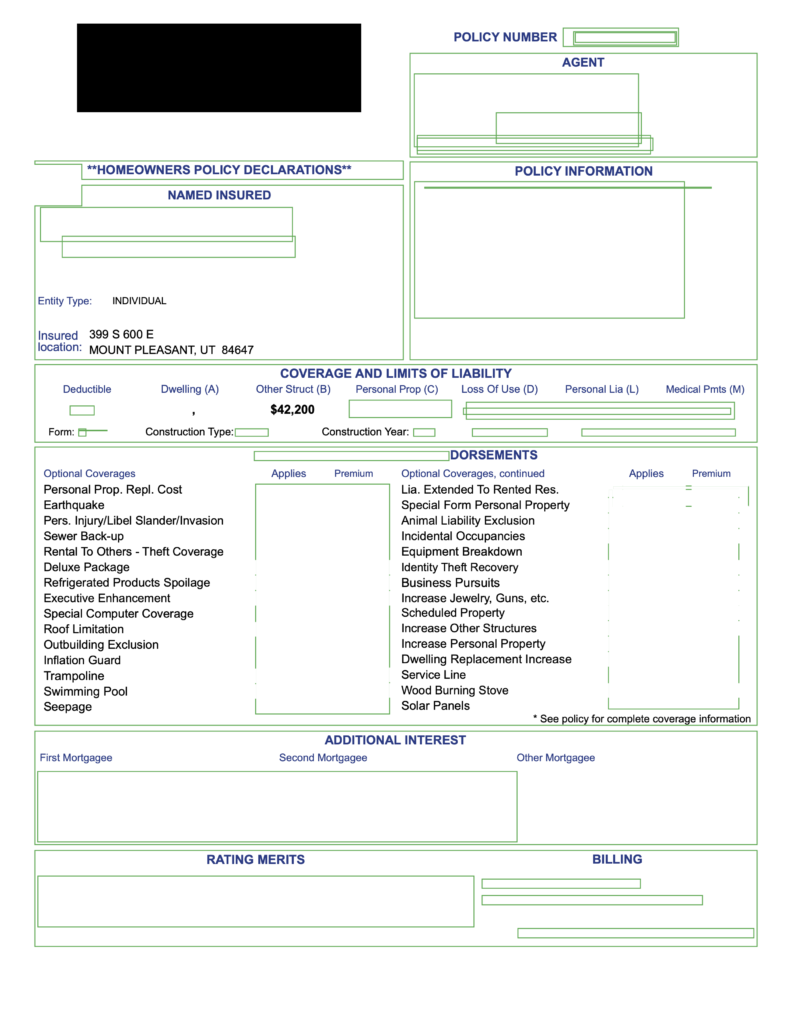

For example, the attached homeowners policy shows Other Struct (B) $42,200 under Coverage and Limits of Liability, meaning the policy includes $42,200 of insurance for other structures on the property.

That is a good example of why homeowners should check the actual declarations page instead of assuming coverage. The policy may already include protection for detached structures, but the built-in amount still needs to be compared to the replacement cost of the new building.

What is Coverage B or Other Structures coverage?

On many homeowners policies, Coverage B is the section that insures structures that are separated from the house. That can include:

- Detached metal garages

- Steel workshops

- Metal storage buildings

- Barns

- RV covers

- Sheds

- Fences and similar detached improvements

The Insurance Information Institute explains that standard homeowners policies often cover detached structures such as a garage, tool shed, or gazebo, generally for about 10 percent of the amount insured on the home.

Why this matters for metal building owners

A newly installed metal building can easily be worth more than a homeowner expects, especially when it includes:

- Larger dimensions

- Vertical roof panels

- Insulation

- Roll-up doors

- Windows and walk doors

- Concrete foundation

- Electrical upgrades

- Interior build-out

- Engineering for local wind load and snow load requirements

A homeowner may have detached-structure coverage built into the policy, but that does not automatically mean the limit is high enough.

In the attached policy example, the homeowner has $42,200 in built-in Other Structures (B) coverage. That may be enough for some detached structures, but a larger custom metal garage, shop, or barn could exceed that amount depending on the size, features, and local rebuilding costs.

What Experts Say

“A lot of the time, homeowners policies already include some coverage for detached buildings on the property, but you should never assume the amount is enough for a new metal building. The smart move is to compare your Coverage B limit to the actual replacement value of the structure.” — Mike Daniels, Owner, Metal Carports and Buildings

What the attached policy tells us

The attached homeowners policy is a strong example of how detached-structure coverage can already exist at no additional cost. Under COVERAGE AND LIMITS OF LIABILITY, it lists Other Struct (B) $42,200.

That supports an important point for homeowners:

Your policy may already cover a detached metal building, but only up to the stated limit.

So if your new steel building would cost $50,000, $60,000, or more to rebuild, then a built-in $42,200 limit may leave a gap. Homeowners should think in terms of rebuilding cost rather than market value when reviewing coverage.

When built-in detached-structure coverage may be enough

In some cases, the included Other Structures coverage may be enough, especially for a smaller:

- Metal shed

- Utility building

- Small detached garage

- Smaller storage building

If the replacement cost of the building is below the policy’s Coverage B amount, the existing homeowners policy may already provide the protection needed, subject to the policy’s terms, exclusions, deductibles, and covered causes of loss.

When you may need more insurance

Built-in detached-structure coverage may not be enough when:

1. The building costs more to rebuild than the policy limit

This is the biggest issue. If the structure would cost more than the policy’s Other Structures amount, the building may be underinsured.

2. The building is used as a shop or for business activity

If the building is used for business, storing business equipment, running a workshop, or revenue-producing activity, the coverage may need to be reviewed more carefully with the insurer.

3. The building contains expensive contents

The building itself is one issue. The tools, vehicles, equipment, inventory, or machinery inside it are another.

4. The structure has been upgraded

Once you add insulation, electrical, plumbing, HVAC, framing, or interior improvements, the replacement value can rise quickly.

5. The building is in a region with higher wind, hail, snow, or wildfire exposure

Local risk can affect underwriting, deductibles, and how the insurer values the structure.

What Experts Say

“We encourage customers to call their insurance company as soon as the building is installed and provide the dimensions, use, features, and total replacement value. A metal building is too important of an investment to leave underinsured.” — Mike Daniels, Owner, Metal Carports and Buildings

What to tell your insurance agent about your metal building

If you want your metal building insurance review to go smoothly, be ready to provide:

- Building dimensions

- Whether it is open, partially enclosed, or fully enclosed

- Whether it is attached or detached

- Use of the structure

- Construction details

- Doors, windows, and insulation

- Electrical and plumbing details

- Concrete slab or foundation information

- Photos of the completed structure

- Invoice or contract amount

- Estimated replacement cost

- Whether the building was engineered for local wind and snow loads

That last point is especially important. A properly engineered structure built for the property’s location is easier to document and explain than a vague or undocumented outbuilding.

For more on planning the right structure, see Building Styles, Design Your Building

, and the FAQ

at Metal Carports and Buildings.

Why engineered metal buildings matter for insurance

Insurance is about documented risk and rebuild value. A custom engineered structure gives a homeowner a better record of what was actually built.

At Metal Carports and Buildings, we help property owners design structures that are engineered and certified for their location, including wind load and snow load requirements where applicable. That matters for planning, permitting, long-term durability, and the insurance conversation after installation.

You can also read related articles such as:

- Pole Barn vs Metal Building: Cost, Durability and Long-Term Value

- What is cheaper, a pole barn or a metal building?

- Is It Cheaper to Build a Metal Building or Wood?

What Experts Say

“One of the biggest insurance mistakes we see is when someone assumes their detached building is fully covered just because it sits on the same property as the home. The declarations page tells the real story.” — Mike Daniels, Owner, Metal Carports and Buildings

Final answer: how do you insure a metal building after it is built?

Start by checking your homeowners declarations page.

Look for Coverage B or Other Structures and see what amount is included. In the attached policy example, that amount is $42,200, showing that detached structures on the property already have coverage built into the policy.

Then ask one critical question:

Would it cost more than that to rebuild the building today?

If the answer is yes, talk to your insurance agent about increasing your detached-structure coverage or otherwise adjusting the policy. If the answer is no, your existing policy may already provide a solid starting point, subject to the full terms of the policy.

The bottom line is simple: many homeowners policies already cover detached metal buildings, garages, shops, and sheds up to a certain amount. The smart next step is making sure that amount actually matches the value of what you built.

FAQ and Q&As

Does homeowners insurance cover a detached metal building?

Often yes. Many homeowners policies cover detached structures under Coverage B or Other Structures, but only up to the policy limit.

What does Other Structures coverage mean?

It usually refers to coverage for buildings and structures on the property that are not attached to the house, such as detached garages, sheds, barns, and workshops.

How much detached-structure coverage did the attached policy include?

The attached policy lists Other Struct (B) $42,200 under Coverage and Limits of Liability.

Is $42,200 enough to insure a metal building?

It depends on the size, design, features, and replacement cost of the building. For some smaller outbuildings it may be enough. For larger custom metal buildings, it may not be.

What should I do after my metal building is installed?

Review your declarations page, document the building, calculate replacement cost, and call your insurance agent to confirm the structure is properly insured.

Why it Matters.

Learn how to insure a metal building after installation. See how homeowners insurance may already cover detached structures, including a real example with $42,200 in Other Structures coverage.

Let us help!

At Metal Carports and Buildings, we design, engineer, deliver, and professionally install certified metal buildings, metal garages, RV covers, steel sheds, and metal barns for property owners in Washington, Oregon, Idaho, Montana, Wyoming, Utah, Colorado, New Mexico, Oklahoma, Kansas, Nebraska, and Texas. Get your free no-obligation quote at MetalCarportsandBuildings.com or call 435-250-4446.